|

Embracing productivity and innovation key to sustaining profitability in besieged retail banking sector

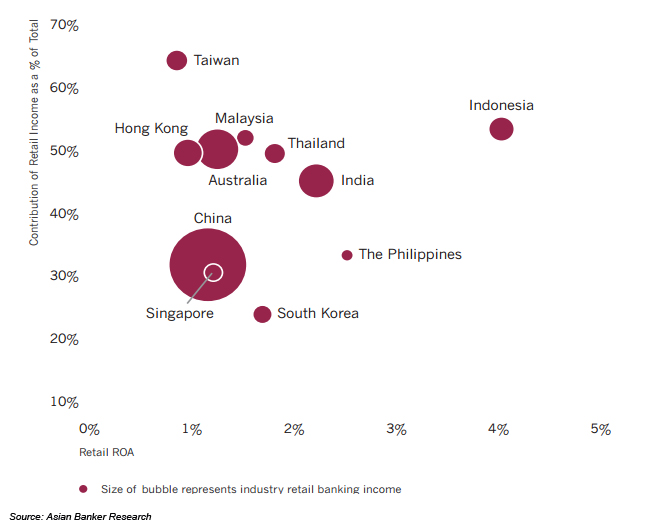

Banks in Asia Pacific are responding to tightening regulations and fee ceilings with creative strategies and more effective business models. July 24, 2013 | ResearchThe last three years saw the introduction of detailed interest and debt ceilings and fee charges for core banking transactions which have in effect obliterated significant profit streams in retail financial services for banks. At the same time, property prices continued to escalate in the region, causing regulators to implement more stringent measures in countries like Hong Kong, Taiwan, Korea, Malaysia and Singapore. In UAE, 2012 saw the full impact of its new consumer regulations introduced in mid-2011 on maximum customer debt-to-income ceiling and fees banks can charge for core banking transactions. The regulator capped the issuance of personal loans at 20 times salary. Aggressive banks were lending at 180 to 240 times salary while the average bank was lending around 80 times salary. We estimate that the retail revenue of UAE retail financial services decreased between 20% and 30% in 2012 and will further contract in 2013. Banks’ return on retail assets have come under pressure Figure 1. Return on assets vs. contribution of retail income to total income

Best retail banks today have a healthy cost to income ratio of around 40% Figure 2. Cost to income ratio vs. contribution of ret...

Categories: Keywords:Bank Baiduri, HSBC Brunei, Standard Chartered Bank Brunei, CIMB, OCBC, UOB, KHFC, Kookmin Bank, Shinhan Bank

|