|

ING Direct Australia an exception in INGs struggling Asia Pacific region business

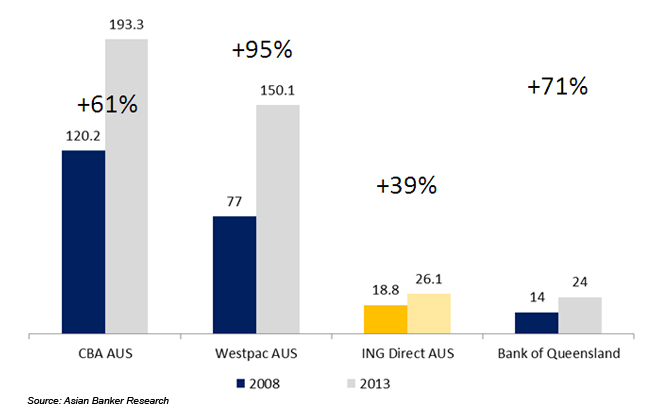

Simplicity in product lines, quality in service, keep ING Direct Australia’s operating profitability high enabling it to maintain an even keep with commercial banks. April 10, 2014 | ResearchSince 2009, ING has been scaling down its commitment in the Asia Pacific region by divesting its asset and insurance business to domestic financial institutions. What was once a sprawling $7 billion business from retail banking to asset management and insurances has been trimmed to a few stakes in India, Thailand and China, with its only ING Direct business being in Australia. ING’s business strategy in consumer banking is based on a developed market retail financial services approach and executed on a direct banking model. It pursues local strategy in the Asia Pacific depending on the maturity of the markets. It entered developing markets such as India and China with established but often insignificant players. Under European Union orders to divest all non-core assets, and partnerships with little upside potential it is also intends selling off some of those minority stakes. ING Group is said to be seeking a buyer for its Indian affiliate, ING Vysya Bank with a stake of 44%. The prospects of limited direct banking in India and tough competition in the retail market makes it rethink its local strategy. Its planned sale of a 31% stake, worth roughly $950m, in Thai Military Bank has been on the block informally since the Dutch banking and insurance group was instructed to split itself up and sell non-core assets but is struggling to find a suitable buyer due to politics, indebtedness of consumers, higher spending levels and currency instabilities. With the impending divestment of its minority stakes in India and Thailand, ING relocated since 2012 high key executives to its Australian franchise. Vaughn Richtor, CEO ING Banking Asia and CEO ING Direct Australia, resumed CEO leadership of the Australian franchise in 2012, after running this franchise already from 1999-2005, and running ING Vysya Bank India from 2006-2012. ING Direct Australia has also named a replacement for CIO Andrew Henderson, with ING veteran Simon Andrews relocating from its Thai affiliate to run the bank’s internal IT and operations. Back then in 1999, when ING Direct Australia launched the Australia’s first branchless banking, it promised to keep things simple for its customers. At that time, it offered only an online savings account. Today, it is the 5th largest retail bank, commanding a 3% core deposit market share and a customer base of over 1.5 million. Its ROE stood at 11% by end 2013. The bank claims it has an industry leading Net Promoter Score of 14.8 based on the Nielsen Financial SM, December 2013, a position has been holding for the last 3 years (with the exception of one quarter). The group has operating segments including; mortgages, savings, superannuation, and commercial loans. Since 2008, it made improvements in key areas such as its core deposit contribution to total funding from 41% to 57% and reduced its expenses from 42% to 35%. To increase its revenue legs and strengthen its core deposit funding, it entered the superannuation market in September 2012, incorporating the first balanced superannuation fund available to all Australians with no administration or management fees. According to ING Direct, it had the fastest growing superannuation product in the market with Living Super growing to 21,000 accounts by December 31, 2013 with funds under management reaching $641m. Yet, despite growing its retail deposits by $6.6 billion between 2008 and 2013, compared to its peers, ING Direct may lack teeth with its deposit growth. Some of the barriers to growth certainly are related to issues of instability spilling over from its parent company in the initial years after the global financial crisis. Branchless banking, may further have contributed to a lower growth in the core deposit business. ING Direct grew retail deposits by $6.6 billion between 2008 and 2013 Fig 1. Retail Deposit Growth by Australian Banks (A$ bn, 2008, 2013)

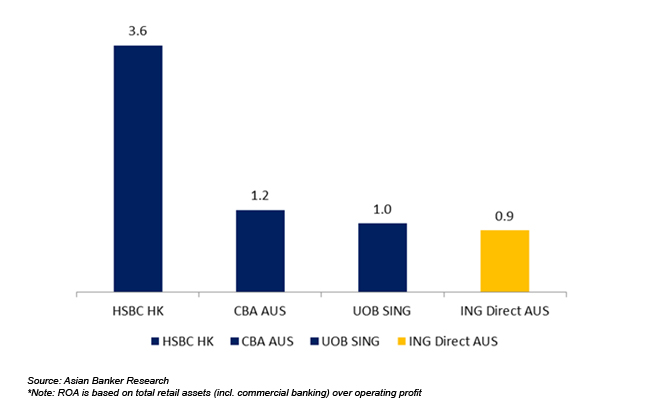

“We ran our own race. We cannot do everything for everybody. If you want complex products or private banking type services, then we leave it for the customers to choose. Our focus is mass market and we want them to have control over their finances. Secondly, when we started out in 1999 we were happy to be a second bank. We couldn’t do everything. Increasingly, though, we would like see our customers having their checking account, their savings and mortgage and their superannuation with us. Today, we are pursuing a primary banking relationship where customer transact, borrow and invest with us. The percentage of active customers with two or more products, including savings accounts, increased from 5% in 2008 to 14% in 2013 indicating that we are on the way becoming a primary bank. We consider ourselves a bank and not an online bank. When we came into this market in 1999 the opportunity we saw was not what everybody else is doing such as branch banking but to do business direct with customers. What we trying to do though to make sure we do not compromise on the service quality. We believe people are patronising branches because call centre services or digital banking does not offer them the high quality service we can offer in Australia. Increasingly people could do everything they need to do online and via mobile banking. And if they need to post a cheque they don’t need to go to a teller now to post a cheque since this can be done by automated cheque readers. Increasingly, we can do everything for our customers digitally. We are a direct bank and most of our interactions are digital today,” says Vaughn Richtor, CEO ING Banking Asia and CEO ING Direct Australia ING Direct maintains close profitability with banks Fig 2. Retail Profitability (ROA) of ING Direct Australia compared to commercial banks

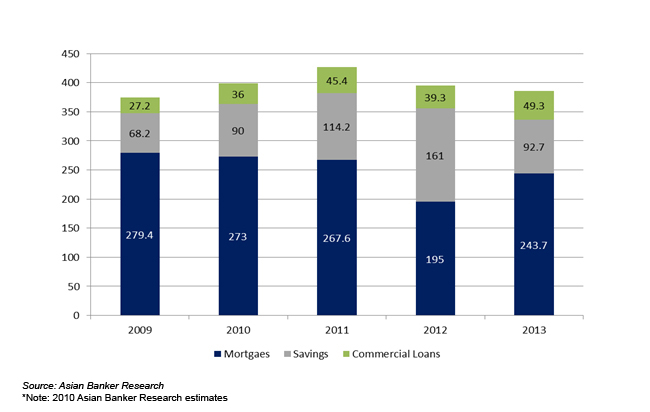

Quality of products and service keep stable profitability Fig 3. Operating Profit of ING Direct Australia (A$, bn) between 2009 and 2013

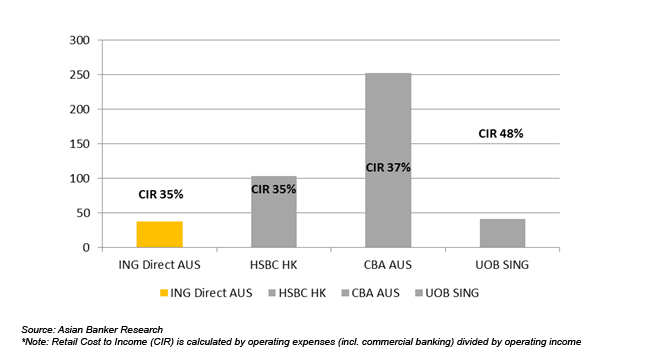

While commercial banks have realised that product complexity and lengthy processes was hurting customer experience ING Direct Australia believed in this strategy form the very outset. “We are really slow introducing new products. In the last 14 years, we had four products being introduced. Basically one product by category, and the reason for that is simple. First of all, products should be discerned to deliver value for the channel it is designed for. There is not point to introduce a product which cannot fit the channel. Secondly, we were able to introduced products where we currently believe we can do better compared to what is currently available. So we don’t try to copy products. And we will continue that way. The critical level is service. The whole thing about financial services in banking is that service is very important for customers but actually it’s complicated. So consumers often get confused as they don’t understand it and on top of that they don’t want to spend a lot of time on it. So, we simplify products. And we simplify the purchase making for the customers. Also, there is no lock in period, you can come and go as often as you like. The only condition is that we don’t have a branch network. By doing so we have sales process which is highly automated and that would delivery benefit to the customers and ourselves. But either way, the simpler the product the better the experience,” explained Richtor. Simplicity keeps low Cost to Income Ratio Fig 4. Size of Retail Assets ($, bn) and Retail Cost to Income Ratio (CIR) 2013

ING Direct’s cost to income ratio of 35% continues to lead the market but it does not highlight the effectiveness of ING Direct bank model in Australia. With the best commercial large scale banks pursuing a leaner and simpler retail banking platform, ING Direct Australia’s CIR need to fall below the 30% to demonstrate a clear differentiation. At the same time it did radically cut back on its miscellaneous expenses, a perennial high cost driver for all commercial banks. ING Direct’ biggest cost drivers are employment and salaries and marketing. Technology currently contributes 5% to total expenses. To strengthen its efficiency strategy and reduce complexity, the bank’s 'Zero Touch IT' streamlining program for its core infrastructure, which will see ING consolidate and simplify a number of platforms into one is currently under way and expected to wrap up end of 2014 which should further yield cost savings. “We responded to making sure that customers have all information about the products. How do we do that? We have a product disclosure statement. The reality is if you have a complex product you have a very complex product disclosure statement which for customers is lengthy and very difficult to understand. So there are two things we try to nourish outside what we do on the product side. At the end of the day technologies allows us to complicate products not always to the benefits for the customers and organisation, because it becomes more complex for the administration,” he adds. While ING Direct certainly offers a strong internet banking proposition with a powerful call centre service, a 3% core deposit market share only in the last 14 years has left industry observers wondering whether a bank can operate without a physical branch network ever in the Australian market. The branch closure of the largest commercial banks in Australia and its repercussions on their brand equity has shown that certain segments among consumers demand branch banking. In fact, during the development of its “Orange Everyday Account” transaction account in 2008/2009, customer research showed that some customer segments preferred a face-to-face transaction for certain services, such as banking cheques and cash. In addition, legislation also required a rigorous identity verification process for all new customers. Eventually, it decided for Australia Post as distribution partner. Since, it has grown its transaction account business to 179,000 transaction accounts as at 31 December 2013, a growth of 34% YoY. Yet, Australia with one of the highest smart phone penetration rates in Asia and the current developments in digital banking, ING Direct might just be sitting in the right spot, if it can execute on its direct banking. The proportion of consumers who own a smartphone grew between September 2011 and 2013, from 49 percent to 68 percent, according to RFi Australian Moibile Payments Council, Sept 2013. Contactless card payments in Australia are showing currently enormous uptake across all age groups above the 24 of age and it is in this space where ING Direct is playing its strength in combination with their popular transaction account. Since ING Directs introduction in 2013 of its payWave service on its “Orange Everyday” the bank has seen strong uptake. The increased usage among ING DIRECT customers is likely due to the bank’s 5% cash back offer on payWave purchases under $100 available for the first six months of holding an account. The use of contactless payments in Australia increased significantly when major grocery chains introduced contactless Terminals. Ownership and usage of contactless cards continued to grow in 2013 across all age groups above 24 of age, the latter driven by the availability of contactless terminals in the two dominant grocery retail chains, Coles and Woolworths, since mid-2012. In the 12 months to September 2013 the proportion of consumers using contactless cards has doubled from 21 percent to 40 percent and is used in particular in supermarkets, petrol stations and liquor stores, according to RFi Australian Mobile Payment Payments Council. A new app was released for iOS and Android devices on 25 June 2013. “By 2013, ING Directs’ mobile banking application was updated with a modernized design with improvements in usability and functionality. The application ensures customers have visibility and control over their personal finances by providing the option to view account balances without logging in. ING has done a great job of incorporating more functionality without breaking any of the existing simplistic user experience. The application was designed with their customers’ needs in mind, placing it in strong competition with ANZ and CBA, says James Breeze, CEO, Objective Digital, a customer experience consultancy. According to the bank its mobile app is now one of the highest rated mobile apps in Australia. The app had a total of 345,000 downloads by the end of 2013, making up around 21% of its total customer base and 2.5% of all smartphone users in Australia (approx. 14 million end of 2013) Categories: Australia, Banks We Like, Customer Centricity, Internet Banking, Mobile Banking, Retail BankingKeywords:Vaughn Richtor, ING Direct Australia, ROE, ROA, Operating Profit |